![]()

1ST QUARTER 2016 MARKET UPDATE: WINTER IS HERE (BUT SPRING ALWAYS FOLLOWS)

1ST QUARTER 2016 MARKET UPDATE:

WINTER IS HERE (BUT SPRING ALWAYS FOLLOWS)

“In the real world, things generally fluctuate between ‘pretty good’ and ‘not so hot.’ But in the world of investing, perception often swings from ‘flawless’ to ‘hopeless.’ The pendulum careens from one extreme to the other, spending almost no time at the ‘happy medium’ and rather little time in the range of reasonableness. The market is manic depressive. It swings from seeing only positives to seeing only negatives and from interpreting everything positively to interpreting everything negatively.” — Howard Marks, Chairman, Oaktree Capital.

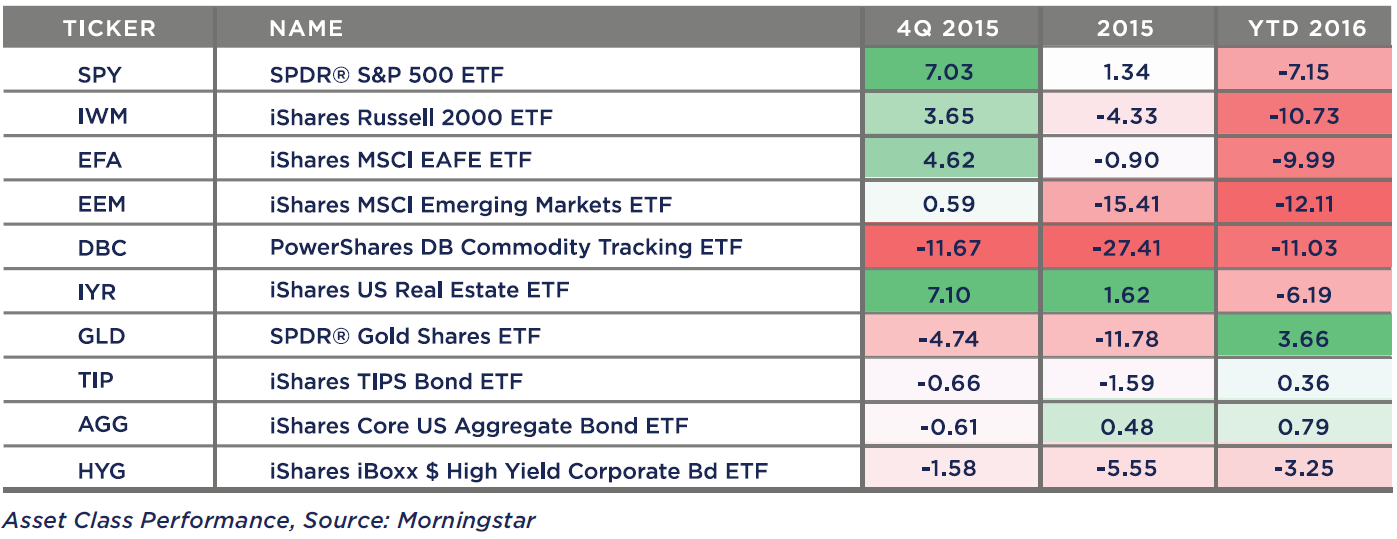

2015 was a challenging year. Evercore ISI strategist Dennis DeBusschere aptly described it as “violently flat.” The S&P 500 closed the year up 1.3%, the US bond market closed up 0.5%, and developed world stock markets were down just 0.9%. Other markets didn’t fare as well: US small cap stocks were down 4.3%, high yield bonds were down 5.6%, gold dropped 11.8%, emerging markets stocks fell 15.4%, and commodities fell 27.4%.

Unfortunately, 2016 started off with the worst opening week in history and global markets have continued their decline for three weeks now.

So, what is driving this extreme volatility? Unfortunately it is impossible to know for sure. It could just be that market excesses are being worked off. Or it could be that one of the following narratives has spooked Mr. Market.

1. China

China is engaged in a massive economic transformation. The state-controlled economy has an objective of moving from an export-driven economy to one similar to the US where a strong middle class can drive the economy forward with domestic consumption. Part of this transition was to encourage investment in the domestic Chinese stock market to create a wealth effect. This worked wondrously for about 18 months as the Shanghai Composite climbed from 2044 at the beginning of 2014 to a high of 5178 in June of 2015 for a gain of over 150%. This kind of exponential growth is never sustainable and the market collapsed by more than 45% in less than three months. After a series of controls were put in place, the Shanghai Composite stabilized and gained about 24% through the end of November. In December, concerns over the viability of Chinese markets resurfaced and the market resumed its fall trading down 19% to the date of this writing. The amazing thing in all of this, to me at least, is that despite all the volatility, the local Chinese market closed the year up about 7.5%. If the US markets were “violently flat,” China was excruciatingly positive. So what does this mean? Despite its economic might, China is still considered an emerging market and, as such, high volatility is not unusual. And while this market volatility is concerning, Chinese stock markets are only loosely associated with the Chinese economy. And, the Chinese economy is what matters. Depending on whether you view Europe as a unit or as independent states, China has the second or third largest economy in the world (behind the European Union and the United States). China’s economic growth is undeniably slowing, but it is not expected to shrink. This is important as China’s growth over the last few years has helped buoy a flagging global economy.

2. Oil

In June of 2014, oil was trading around $100 a barrel. Today it is below $30 a barrel. This collapse in price is due to a perfect storm of conditions. First, in an attempt to derail US production, Saudi Arabia and OPEC decided to maintain production in the face of building supplies and falling prices. Second, slowing growth in China and Europe has led to weakening demand. And third, business, manufacturing, and transportation are in a bit of a renaissance, becoming more and more energy efficient by the day - further decreasing demand. In the short run, falling oil prices generally signal deteriorating global economic conditions. In the longer-run, cheap energy typically contributes to economic prosperity.

3. The Federal Reserve

In December, the FED raised interest rates for the first time in nearly a decade. While the change was minor (from a range of 0.00% – 0.25% to a range of 0.25% – 0.50%), many questioned the wisdom of the hike in the face of weakening global eco-nomic conditions. On the plus side, the Fed clearly believes that the US economy is strong enough to sustain a rise in rates.

Humans evolved over thousands of years and for much of that time the only way to share knowledge and experience was through story telling. For that reason, we all love a good narrative. We like to believe that we can translate our experience and knowledge into better investment results. Unfortunately, markets are extremely complex, wildly unpredictable, and rarely follow the scripts that we create. So, while all of the above storylines are interesting and to some degree valid, they probably don’t fully explain what we have witnessed in the last year.

Ben Graham, the father of value investing, said this: “In the short-term the market is a voting machine, but in the long-run, it is a weighing machine.” This seems to have never been truer than today, as automated trading programs drive prices up and down far more rapidly than fundamentals would ever suggest. In the long-run though, what matters is the health of economies and the corporations we invest in. We continue to see and expect slow but moderate growth. Unlike in 2008, life support systems are not on standby.

SO WHAT ARE WE THINKING ABOUT AT SIGNAL RIDGE?

1. Volatility

After years of below average volatility, the CBOE volatility index spiked in August and has remained elevated ever since. From our perspective, volatility in and of itself is not bad and is often the source of opportunity. However high volatility is always unsettling. For this reason, managing volatility is one of our core concerns. One of the biggest reasons that investors fall short of their goals is that they bail on sound investment strategies at exactly the wrong time. Our process focuses on managing volatility and generating adequate risk-adjusted returns over full market cycles.

2. Income

While the Fed did raise interest rates in December, this increase is unlikely to result in much relief to income seekers. Further, with the 10-year treasury once again below 2%, safe income is difficult to find. High yield has recently become interesting for a couple of reasons. First, high yield has historically weathered periods of rising rates better than higher quality, lower yielding bonds. Second, the premium that you receive for investing in these riskier bonds is about 33% higher than the long term average. We typically access this asset class through a fund that buys high yield closed-end funds at discounts, further enhancing the income opportunity.

3. Bond markets

Interest rates have been on a steady decline since the early 1980s. As rates fall, the principal values of bonds typically rise. So for the last 35 years, bond investors have enjoyed total returns consisting of yield plus asset appreciation. If we have truly entered a period of sustained rising rates, this tailwind is gone and bond yields today are not high enough (2% or less) to provide significant returns to portfolios. All this said, we have reviewed past periods of rising rates, and while we don’t expect high returns from bonds we do expect them to continue to perform positively in difficult markets such as the one we are dealing with today. Our expectation is that bond markets will be more volatile in future years and we have thus made two adjustments to portfolios. First, we have limited our exposure to long-dated bonds as these will be most adversely affected by any interest rate increases. Second, we have employed two low-cost, active managers to attempt to build a stable core for portfolios while maintaining the capacity to capitalize on any opportunities that might arise from uncertain markets.

4. Portfolio construction

2015 was a difficult year for diversified portfolios. An equally weighted portfolio consisting of Facebook, Amazon, Netflix and Google was up about 83% last year. But a more reasonable portfolio of 500 of the largest companies in the United States was up just 1.3% (including dividends!). If you added bonds to your portfolio, your return was lower but still positive. But once you started to build a complete portfolio including global stocks and bonds, returns turned negative. A respected institutional chief investment officer, Wharton professor, and acknowledged expert on asset allocation runs a series of thoughtfully constructed, globally diversified portfolios that we watch. He runs several models that we think are good comparisons to what we do. His Risk-Balanced Model that is most similar to our investment style was down 8.9% for the year. While we are happy to report that all portfolios outperformed this benchmark, it does point to just how difficult a year 2015 was. Signal Ridge was founded on the view that we don’t want our clients to experience the massive losses associated with equity bear markets that happen all too frequently. That’s why we build globally diversified portfolios that have the capacity to adapt to changing market conditions.

5. Enhanced opportunity set

For over a year now, we have been harping on high valuations implying low future returns. We would prefer that markets climb steadily in perpetuity, though that would eliminate the need for our guidance. In reality though, bear markets are a relatively common phenomenon. Throughout history they have occurred every five to seven years. So after more than six years of uninterrupted advances from the 2009 bottom you could say we were due for this. And while we find these conditions just as painful as you do—perhaps more so since we spend our days fully immersed in the noise and turbulence —they do result in an improved global investment opportunity set. After the turmoil of the last year, virtually every asset class (save government bonds) is cheaper. In the long-run, the price you pay for something most certainly matters. It is a mathematical truth that the less you pay today, the higher your return on that investment will be.

“In terms of available returns, dispersion of returns, and stability of returns, 2015 presented a more challenging environment than almost any year in the past two decades. In aggregate (these conditions) presented a perfect storm, which resulted in performance across many strategies that was well below long-term expectations. While we can offer no guarantee that the situation will improve (in 2016), our confidence is bolstered by the knowledge that in markets, it is almost always darkest before the dawn.”

— Michael Philbrick, President, Resolve Asset Management

We are committed to providing you with the highest quality service, planning, and investment management available. If you have any questions or concerns, or if your personal circumstances have changed, please let us know.

Sincerely,

DISCLOSURES:

This presentation is not an offer or a solicitation to buy or sell securities. The information contained in this presentation has been compiled from third party sources and is believed to be reliable; however its accuracy is not guaranteed and should not be relied upon in any way, whatsoever. This presentation may not be construed as investment advice and does not give investment recommendations. Any opinion included in this report constitutes the judgment of Signal Ridge Capital Partners (Signal Ridge) as of the date of this presentation, and are subject to change without notice. Additional information, including management fees and expenses, is provided on Signal Ridge’s Form ADV Part 2. As with any investment strategy, there is potential for profit as well as the possibility of loss. Signal Ridge does not guarantee any minimum level of investment performance or the success of any portfolio or investment strategy. All investments involve risk (the amount of which may vary significantly) and investment recommendations will not always be profitable. The investment return and principal value of an investment will fluctuate so that an investor’s portfolio may be worth more or less than its original cost at any given time. The underlying holdings of any presented portfolio are not federally or FDIC-insured and are not deposits or obligations of, or guaranteed by, any financial institution. Past performance is not a guarantee of future results. Presentation is prepared by: Signal Ridge Capital Partners